All Categories

Featured

Table of Contents

Keep in mind, however, that this does not state anything regarding adjusting for rising cost of living. On the plus side, even if you assume your choice would be to purchase the stock exchange for those seven years, and that you would certainly obtain a 10 percent yearly return (which is much from certain, specifically in the coming years), this $8208 a year would certainly be greater than 4 percent of the resulting small supply worth.

Example of a single-premium deferred annuity (with a 25-year deferral), with 4 payment alternatives. Politeness Charles Schwab. The regular monthly payout below is greatest for the "joint-life-only" option, at $1258 (164 percent greater than with the prompt annuity). Nevertheless, the "joint-life-with-cash-refund" option pays just $7/month much less, and guarantees at the very least $100,000 will be paid.

The method you buy the annuity will figure out the response to that concern. If you purchase an annuity with pre-tax bucks, your costs reduces your taxable income for that year. According to , buying an annuity inside a Roth plan results in tax-free payments.

Is there a budget-friendly Tax-deferred Annuities option?

The advisor's very first action was to create a thorough financial plan for you, and afterwards discuss (a) just how the proposed annuity matches your overall plan, (b) what choices s/he considered, and (c) how such alternatives would certainly or would not have actually caused lower or higher payment for the advisor, and (d) why the annuity is the superior choice for you. - Lifetime payout annuities

Of training course, an expert may try pressing annuities even if they're not the very best fit for your situation and objectives. The reason could be as benign as it is the only item they offer, so they drop victim to the typical, "If all you have in your tool kit is a hammer, pretty soon every little thing begins resembling a nail." While the advisor in this situation might not be dishonest, it raises the risk that an annuity is a bad option for you.

How do I apply for an Annuity Income?

Given that annuities often pay the agent selling them much higher payments than what s/he would receive for investing your money in common funds - Secure annuities, not to mention the zero commissions s/he would certainly get if you spend in no-load mutual funds, there is a large reward for representatives to push annuities, and the a lot more challenging the far better ()

An unethical consultant suggests rolling that quantity into brand-new "better" funds that just take place to lug a 4 percent sales tons. Consent to this, and the consultant pockets $20,000 of your $500,000, and the funds aren't likely to carry out much better (unless you selected much more improperly to start with). In the very same example, the expert can guide you to get a complex annuity keeping that $500,000, one that pays him or her an 8 percent payment.

The consultant hasn't figured out how annuity repayments will be exhausted. The advisor hasn't divulged his/her compensation and/or the costs you'll be charged and/or hasn't shown you the impact of those on your ultimate repayments, and/or the payment and/or fees are unacceptably high.

Current interest rates, and therefore forecasted payments, are traditionally low. Even if an annuity is right for you, do your due persistance in contrasting annuities marketed by brokers vs. no-load ones marketed by the issuing business.

What are the tax implications of an Annuity Interest Rates?

The stream of monthly payments from Social Safety and security is comparable to those of a delayed annuity. A 2017 relative evaluation made an in-depth comparison. The following are a few of the most prominent factors. Because annuities are voluntary, the individuals acquiring them normally self-select as having a longer-than-average life span.

Social Safety and security benefits are completely indexed to the CPI, while annuities either have no rising cost of living security or at many offer an established percentage yearly increase that may or may not make up for inflation in full. This sort of motorcyclist, just like anything else that boosts the insurance provider's risk, needs you to pay more for the annuity, or approve lower payments.

How can an Annuity Income protect my retirement?

Disclaimer: This write-up is meant for educational purposes only, and should not be thought about financial recommendations. You ought to speak with a financial professional before making any kind of major financial choices.

Considering that annuities are intended for retired life, tax obligations and charges may apply. Principal Protection of Fixed Annuities.

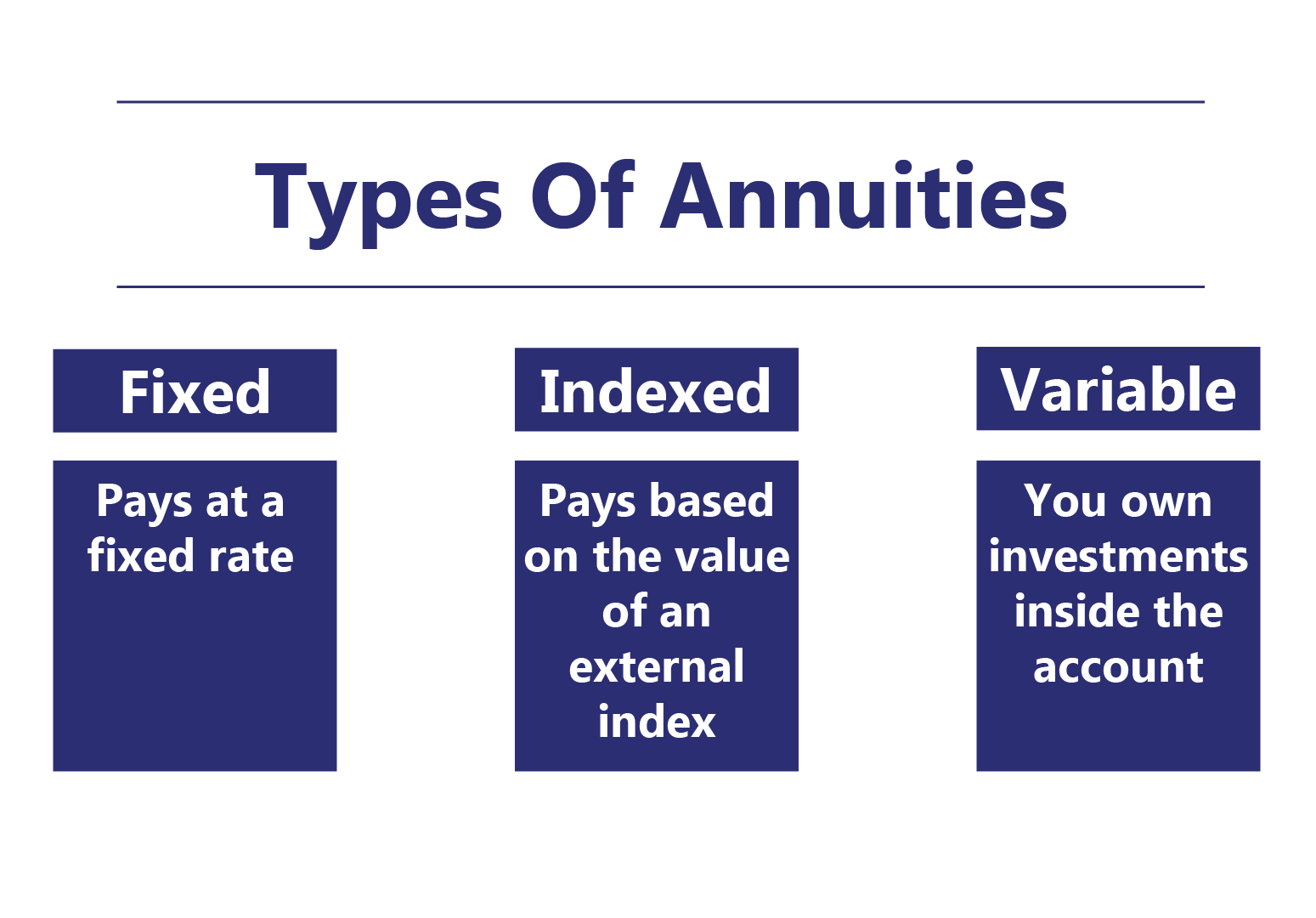

Immediate annuities. Utilized by those who want dependable earnings right away (or within one year of acquisition). With it, you can customize revenue to fit your needs and create earnings that lasts forever. Deferred annuities: For those who want to grow their cash in time, yet want to postpone accessibility to the cash up until retired life years.

Is there a budget-friendly Retirement Annuities option?

Variable annuities: Offers better potential for growth by spending your cash in investment alternatives you choose and the capacity to rebalance your portfolio based upon your choices and in a manner that aligns with altering financial objectives. With fixed annuities, the business invests the funds and offers a rate of interest to the customer.

When a fatality case accompanies an annuity, it is essential to have a named recipient in the agreement. Various alternatives exist for annuity survivor benefit, relying on the agreement and insurance provider. Choosing a reimbursement or "period particular" choice in your annuity offers a fatality benefit if you die early.

How do I cancel my Tax-deferred Annuities?

Calling a recipient other than the estate can aid this procedure go a lot more efficiently, and can help ensure that the earnings go to whoever the specific desired the cash to go to rather than going with probate. When present, a death benefit is instantly consisted of with your contract.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Variable Vs Fixed Annuity Key Insights on Fixed Index Annuity Vs Variable Annuities Breaking Down the Basics of Fixed Vs Variable Annuities Advantages and Disadvantages of Different Reti

Decoding Fixed Interest Annuity Vs Variable Investment Annuity A Closer Look at How Retirement Planning Works Defining Pros And Cons Of Fixed Annuity And Variable Annuity Pros and Cons of Various Fina

Highlighting the Key Features of Long-Term Investments Key Insights on Your Financial Future What Is Fixed Income Annuity Vs Variable Annuity? Benefits of Deferred Annuity Vs Variable Annuity Why Choo

More

Latest Posts